Delving into the realm of home insurance coverage types opens up a world of protection and security for homeowners. Understanding the various options available can make all the difference in safeguarding your most valuable asset. Let’s navigate through the intricate details of home insurance coverage types to ensure you have the right protection in place.

Types of Home Insurance Coverage

When it comes to protecting your home, having the right insurance coverage is essential. There are different types of home insurance coverage available to homeowners, each offering varying levels of protection. It’s crucial to understand the options and choose the coverage that best suits your needs.

Basic Coverage

Basic home insurance coverage typically includes protection for your home’s structure and personal belongings against common risks like fire, theft, and certain natural disasters. While basic coverage offers a fundamental level of protection, it may have lower coverage limits and fewer benefits compared to standard or comprehensive policies.

Standard Coverage

Standard home insurance coverage builds upon basic coverage by offering additional protection for liabilities, such as personal injury claims on your property, and may include coverage for additional risks like water damage. Standard policies often have higher coverage limits and more extensive benefits than basic coverage, providing a more comprehensive level of protection.

Comprehensive Coverage

Comprehensive home insurance coverage is the most extensive option available, offering protection for a wide range of risks, including accidental damage to your property and personal belongings. Comprehensive policies typically have higher coverage limits, more benefits, and may include additional features like loss of use coverage to help with living expenses if your home becomes uninhabitable.It is essential for homeowners to have the right combination of coverage to ensure adequate protection for their home and possessions.

Understanding the differences between basic, standard, and comprehensive coverage options can help you make an informed decision when selecting the right insurance policy for your needs.

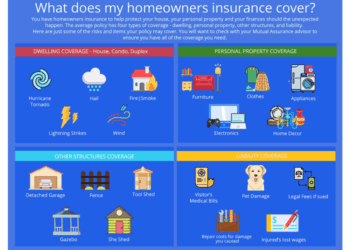

Dwelling Coverage

Dwelling coverage is a fundamental component of a home insurance policy that protects the physical structure of your home, including the walls, roof, foundation, and attached structures, from covered perils such as fire, windstorm, and vandalism. It provides financial protection in case your home is damaged or destroyed, allowing you to repair or rebuild your property.

What’s Typically Included

- Structure of the Home: Covers the main building and any attached structures like a garage or deck.

- Foundation: Protection for the foundation of the home.

- Roof: Coverage for damage to the roof caused by covered perils.

- Interior and Exterior Walls: Includes repairs or replacement of walls damaged by covered events.

- Built-in Appliances: Coverage for appliances like built-in ovens or refrigerators.

Factors Affecting Coverage Amount

- Home Value: The cost to rebuild your home plays a significant role in determining the amount of dwelling coverage needed.

- Location: Areas prone to natural disasters or high crime rates may require higher coverage limits.

- Age of Home: Older homes may need more coverage due to the potential cost of repairing or replacing outdated materials.

- Construction Materials: The type of materials used in your home’s construction can impact the cost of rebuilding and, therefore, the coverage amount.

Determining Appropriate Coverage

- Get a Professional Appraisal: Hire a professional appraiser to assess the value of your home and recommend the appropriate coverage amount.

- Consider Replacement Cost: Opt for replacement cost coverage to ensure you can rebuild your home with similar materials and quality in case of a loss.

- Review Regularly: Periodically review your dwelling coverage limits to account for any changes in home value or improvements you’ve made to the property.

Personal Property Coverage

When it comes to home insurance, personal property coverage is a crucial aspect that protects your belongings in case of damage or theft. This coverage typically extends to items inside your home, such as furniture, electronics, clothing, and other personal possessions.

Examples of Items Covered

- Electronics (TVs, laptops, smartphones)

- Furniture (sofas, beds, dining tables)

- Clothing and accessories

- Jewelry and watches

- Appliances (washing machines, refrigerators)

- Sporting equipment (bicycles, golf clubs)

- Artwork and collectibles

Importance of Creating a Home Inventory

Creating a home inventory is essential for personal property coverage as it helps you keep track of your belongings and their value. In the event of a loss, having a detailed inventory can streamline the claims process and ensure that you receive proper compensation for your items.

Strategy for Adequate Coverage

- Take inventory: Document all your belongings, including descriptions, receipts, and photos.

- Regular updates: Review and update your home inventory annually or as you acquire new items.

- Appraisal: For high-value items like jewelry or art, consider getting professional appraisals to ensure accurate coverage.

- Review policy limits: Make sure your personal property coverage limits are sufficient to replace all your belongings in case of a total loss.

- Add endorsements: Consider adding endorsements to your policy for specific items that may need additional coverage, such as expensive electronics or jewelry.

Liability Coverage

When it comes to home insurance, liability coverage is a crucial component that protects homeowners in case someone is injured on their property or if they accidentally damage someone else’s property.

Coverage Limits and Scenarios

- Liability coverage typically starts at around $100,000 but can be increased to $300,000 or more depending on the policy.

- Scenarios where liability coverage applies include slip and fall accidents, dog bites, or if a tree from your property falls onto your neighbor’s house.

- It also covers legal fees if you are sued for damages caused to others.

Financial Protection

- Liability coverage protects homeowners financially by covering medical expenses, legal fees, and repair costs for damaged property.

- It provides peace of mind knowing that you are financially protected if an unfortunate event occurs on your property.

- Without liability coverage, homeowners could face significant financial losses if they are found liable for injuries or damages.

Selecting the Appropriate Limit

- It is important to assess your assets and determine the appropriate liability coverage limit based on your financial situation.

- Consider factors such as the value of your home, savings, and other assets that could be at risk in a lawsuit.

- Consult with your insurance agent to understand the implications of different coverage limits and choose the one that provides adequate protection for your needs.

Final Conclusion

In conclusion, home insurance coverage types play a crucial role in providing financial security and peace of mind for homeowners. By choosing the appropriate combination of coverage options, you can rest easy knowing that your home and belongings are safeguarded against unexpected events.

Stay informed, stay protected.

Essential Questionnaire

What is the difference between basic, standard, and comprehensive coverage?

Basic coverage offers minimal protection, standard coverage provides a moderate level of protection, and comprehensive coverage offers extensive protection for various risks.

How can homeowners determine the appropriate dwelling coverage for their specific home?

Homeowners should consider factors such as the home’s value, location, and construction type to determine the right amount of dwelling coverage needed.

Why is creating a home inventory important for personal property coverage?

Creating a home inventory helps homeowners keep track of their belongings and ensures they have adequate coverage in case of loss or damage.

What scenarios does liability coverage typically apply to?

Liability coverage usually applies to incidents where the homeowner is legally responsible for injuries or property damage to others.

{kind=link}